"Why I don't put too much importance on growth" - Rakesh jhunjhunwala (India's Big bull)

Rakesh Jhunjhunwala’s success was built on patience, conviction, and letting winners run. He stressed the importance of valuation, warning against overpaying for growth. His approach to portfolio concentration was simple—let it happen naturally as multibaggers emerge. Above all, he believed in India’s growth story, urging investors to recognize its long-term potential.

LEARNINGS FROM THE MASTERS

Arya H Parekh

2/9/20259 min read

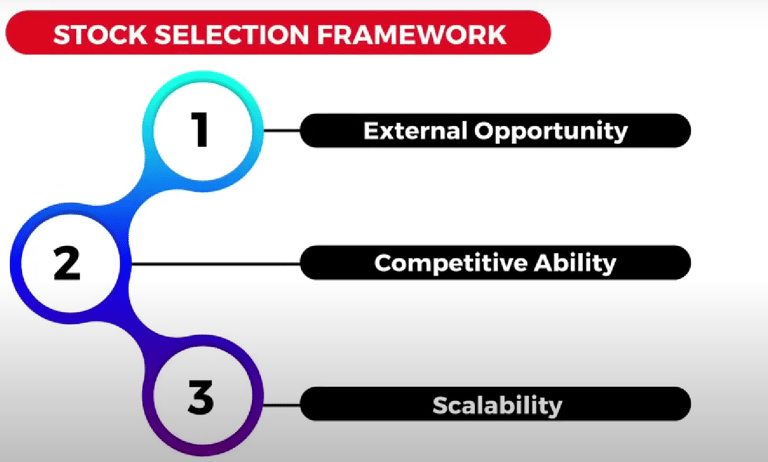

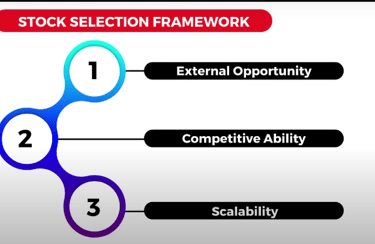

1. The Three Gems of Investing

Three key factors that Rakesh Jhunjhunwala considered when selecting a company were external opportunity, competitive ability, and scalability.

i) External Opportunity

The first thing Rakesh Jhunjhunwala looked for during identifying companies is a Huge External Opportunity. Every industry has its own external opportunity and every industries grows at different rates. External opportunity is also called Total addressable market (TAM) with its Industry growth rate.

Mr Jhunjhunwala believed that even a struggling company could transform if it operated in a sector with significant growth potential. A prime example is Titan,as most of the people don't know that the titan which considered to be as best consistent compounder was considered one of the worst-performing stocks in late 90s. However, Rakesh foresaw the upcoming shift from an unorganized to a branded jewelry market (i;e from 5% branded market to 15-20% branded market) and recognized Titan’s potential to lead this transformation, this also refer as Value migration, which will be discussed in some separate article.

The key for investors is to develop a vision for identifying future external opportunities. To achieve this, they need two essential qualities:

Observation –The ability to notice trends, patterns, and subtle shifts in the market or in your day to day life.

The Power of Imagination – The foresight to visualize how these changes could shape the future and can impact this business, this is also know as Second order thinking.

Imagination, in particular, is a crucial mental model that allows investors to see beyond the present and anticipate long-term potential

Also, It’s equally important to avoid businesses in declining or niche industries with limited growth potential, as they often turn into value traps. Understanding the size of the opportunity is crucial when evaluating investments. If you’d like to dive deeper into this concept, check out our article on learnings from Bharat Shah

Stay in sunrise industry at any cost and stay out of sunset industry at any cost - Vijay Kedia

ii) Competitive Ability

Having an external opportunity is not enough; a company must also possess some sort of competitive edge to capitalize on it. To assess this, an investor must have to develop a deep understanding of the business and industry—only then he/she can determine whether a company has what it takes to survive and thrive in the long run. For example, there are many industries (like construction) has huge external opportunity to expand but most of the companies in this sector, don't have any kind of competitive advantage to stand out.

A company’s competitive strength/Moats depends on factors such as brand power, cost advantages, innovation, and the ability to sustain profit margins etc. So,question an investor should ask or analyze before investing in a particular stock are:

How the company differentiates itself from competitors—Does it offer unique products, superior service, or a strong brand identity?

Its cost structure—Can it produce goods or services more efficiently than rivals, giving it a pricing advantage?

Innovation and adaptability—Is the company investing in new technologies or business models to stay ahead?

Profit sustainability—Does it have the pricing power and customer loyalty to maintain stable earnings even in tough times?

Companies with strong competitive ability can withstand market fluctuations, fend off competition, and ensure long-term business survival. Without this, even a company in a high-growth industry may struggle and eventually fail. As many times what happen is that companies grow very fast but they don't have good ROE & ROCE because of not having any kind of strong competitive edge - "Good growth with poor ROE and ROCE,Means no competitive edge".

"It's important how long it gets, But it's more important how long it lasts" - Rakesh Jhunjhunwala

iii) Scalability and Integrity

I think scalability is very important because companies do not necessarily grows when they get bigger" - Rakesh Jhunjhunwala

Even if a company has market potential and competitive strength, it must also be capable of scaling efficiently. Scalability means expanding operations while maintaining profitability and operational efficiency. Additionally, integrity plays a crucial role—companies with strong governance, ethical management, and transparent financials tend to be more sustainable in the long run.

2. Knowing the Value of the Company

"The first thing we need to realize as investors is that we often know the price of everything but the value of nothing." - Rakesh Jhunjhunwala

Investing is a process of discovery. Markets constantly fluctuate, creating a perception of value that may not align with reality. The key responsibility of an investor is to determine whether the price of a stock reflects its intrinsic value. This requires continuous analysis, patience, and a deep understanding of business fundamentals.

Successful investors always seek to identify mispriced opportunities and avoid being misled by market noise. Knowing the true value of an asset allows investors to make rational decisions rather than emotional ones, especially during tough times. The person who knows the value of a company is the one who can hold the stock for a very long period of time.

But What is Value of Company basically ?

You guessed it right, it is present value of future cash flows but according to Mr. Jhunjhunwala’s philosophy - Value is nothing but a perception—an adjective.

Like If someone is buying a stock thinking there is value in it, then there is always someone who is selling the same stock thinking there is no value in it. It’s also possible that for one person, a stock is not good at five times earnings but is considered good at 20 times its P/E ratio. For Rakesh sir, the most important factors are opportunity and understanding the business model. If you clearly understands the business model and able to see the opportunity a company has in the future and compare it with the current market valuation, you will get an idea of what's the true value of a business should be.

Let’s take the case of McDowell. They have 40% market share of India’s liquor industry. Rakesh said that -

"At the price I was getting it, its market capitalization was about Rs 200cr. It was incredulous. For Rs 200cr you could buy 40% of India’s liquor industry, an industry with great entry barriers. So, I invested in McDowell without spending much time on further investigation."

3. Valuation comes before everything else

Once one has examined the above three aspects of the business and one has found probable avenues to invest in, one needs to decide whether or not to invest.For Rakesh, its is not important what you buy. Its at what price you buy.

I don't put too much importance on growth

For him valuation comes before everything else. He does not likes to put too much not put too much importance on growth.Growth is important, but it is not the only parameter in the valuation.It is just one in several parameter of valuation. He tend to look for greater margin of safety, not only in the respect of growth but also in terms of absolute assets and sustainability/survival of the company. Lets see what he has tell about this -

RAKESH JHUNJHUNWALA: "Well, I don’t necessarily buy a business because it is below book value or sell a business because it is above book value. But I think that with the risk—free interest rate not being higher than 14%, which is very liberal, a business has to be valued at 7 times future sustainable pre-tax cash flows. That’s because a 14% rate of interest gives you a discounting factor of higher than 7".

Premium on Growth Always Falls

Markets often overpay for high-growth stocks, especially during bullish phases. However, the premium attached to growth inevitably declines over time. Many young analysts make the mistake of extrapolating exceptionally high growth rates into their valuation models, leading to unrealistic expectations.

Investors who chase expensive stocks purely based on growth often face sharp corrections, which violates the fundamental objective of investing - The safety of capital. It should always be the only holy objective.

So to handle this, he focuses on opportunities with significant upside potential while ensuring a sufficient margin of safety—where my capital remains well-protected. Valuation discipline is crucial to avoid falling into the trap of overpaying for growth.Therefore, Always buy only when there is sufficient margin of safety available.

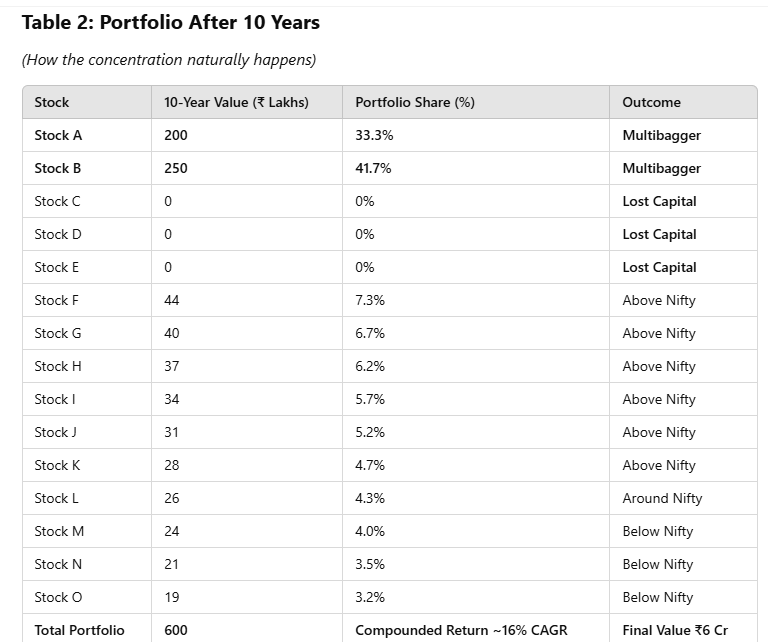

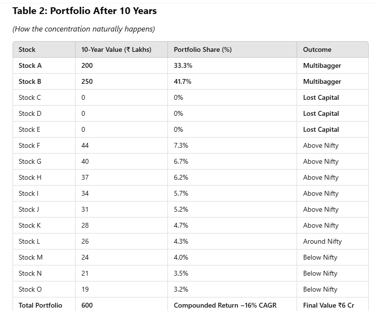

4. Concentration is result of huge winners

One of the biggest mistakes investors make is trying to force concentration too early by heavily investing in a handful of stocks from the beginning year of their investment. However, true concentration is not something you plan—it naturally evolves as your winners grow over time.

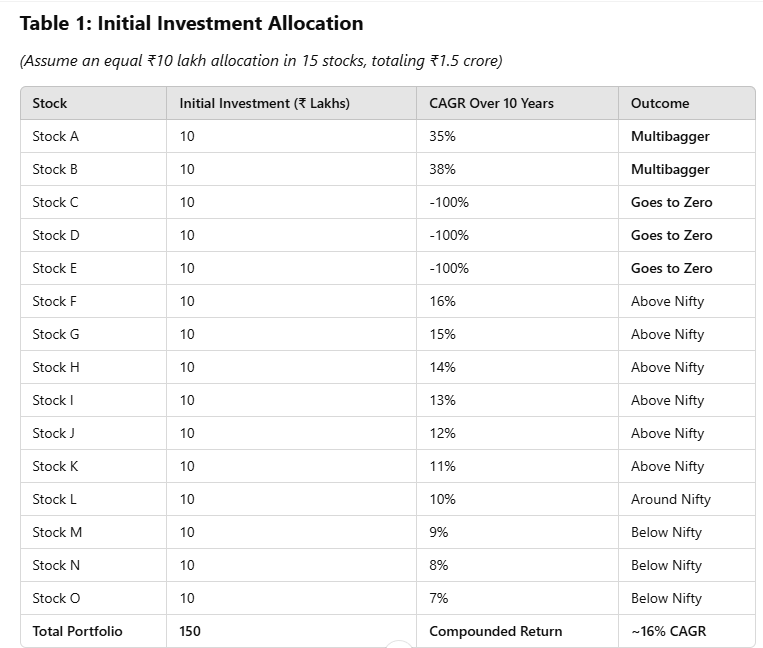

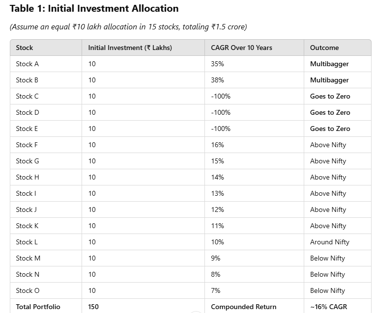

Rakesh Jhunjhunwala emphasized this principle, explaining that when you hold 15 to 20 stocks in your portfolio, you don’t need to deliberately concentrate on any one stock. Instead, concentration is a byproduct of your biggest winners. Over time, a few exceptional stocks will significantly outperform, eventually making up a large portion of your portfolio. Lets take a conservative example -

Multibagger stocks (A & B) naturally became 75% of the portfolio without any forced concentration.

Three stocks went to zero, but the portfolio still delivered strong returns because winners outweighed losers.

A classic example is Titan. Many believe Jhunjhunwala always had a massive allocation to Titan, but that wasn’t the case. Initially, his investment in Titan was relatively small. However, by holding onto it for years, the stock delivered exponential returns, growing to nearly 30-35% of his portfolio. This illustrates the power of letting winners run rather than trying to predict which stocks will dominate from day one.

"Concentration is a result of letting a huge winner run"

The key takeaway? Instead of forcing concentration from your initial year, focus on identifying great businesses and allowing time to show their performance for a long period. If you hold high-quality stocks long enough, your portfolio’s concentration will take care of itself

5. Eternal optimism on India

Where Is the Money? I Say, Where Are the Shares?

Many people often ask, “Where is the money?” when it comes to the stock market. However, Rakesh Jhunjhunwala had a different perspective—he believed the real question should be, “Where are the shares?”He pointed out that India has household savings of 25% of GDP, yet less than 2% of those savings flow into the stock market. He believed that over time, this number could reasonably rise to 5%. When that happens, demand for stocks will surge, but supply—the number of companies available to invest in—remains limited. Since companies cannot be created overnight, the scarcity of investable stocks will drive valuations higher.

Fiscal Deficit < Savings Strength

When asked whether India’s fiscal deficit was a concern, Jhunjhunwala dismissed it. He argued that India’s savings far outweigh its fiscal deficit. At the time, Indians were saving ₹7–7.5 lakh crores annually, while the fiscal deficit stood at just ₹2 lakh crores. This strong savings rate provided stability to the economy and markets.

Pharma: A Huge Opportunity for India

Among sectors, Jhunjhunwala was most bullish on the pharmaceutical industry, particularly the second-line pharma companies with strong potential for global expansion. He believed that:

Global entry barriers in pharma are high, making it a lucrative industry.

The U.S. spends 17% of its GDP on healthcare, ensuring a strong demand for medicines.

Unlike other industries, pharmaceuticals won’t face tariffs from the U.S., making India a strong sourcing base for global markets.

Global Investments in India

The growing interest of foreign investors in India further reinforced his bullish stance. BlackRock, one of the world’s largest asset managers, had announced plans to double its investment in India, which at the time made up only 5% of its portfolio. This was a sign that global institutions were recognizing India’s long-term potential.

Bullish on India’s Economy and Markets

"I am bullish on the Indian stock market but I am more bullish on India’s economy".

There is an important learning that I found when I looked at the old investors like Rk damani, Ramesh Damani, Rakesh Jhunjhunwala, Durgey Shah - the first thing which is common among all of them is all of them are Always bullish on India.

Jhunjhunwala’s final message was clear: Investment conviction is crucial. Have belief and faith in the market. India’s economic strength, rising domestic savings, and increasing global interest made it a promising destination for long-term investors.

Late Rakesh Jhunjhunwala was one of the better known equity investors in India. Mr. Jhunjhunwala has been profiled as one of India’s best five investors by Business India magazine in 1998. Over 39 years, he delivered an astonishing 52% CAGR of returns, a feat few can match. As a long term investor,Mr. Jhunjhunwala was credited for his vision & his ability to see the future which helps him in identifying stocks early on, believing in his investment, being patient and having conviction to hold the stocks for long periods of time. Here are the the top 5 lesson which we can apply in our investment journey.

So lets get start -

"This blog draws inspiration from Rakesh jhunjhunwala's insightful interview (mainly by Indian Money Monarch). We hope these timeless lessons empower you to navigate your investing journey with wisdom, make well-informed decisions, and build enduring wealth. Here’s to thoughtful investing and lasting success — Happy investing!"

Investing & Finance

Develop the Right mindset of investing in the indian stock market from the masters.

contact - arya@masterinvesting.in

© 2024. All rights reserved.